Stablecoin products often look simple from the outside. A user sees a dollar balance, a send button, a checkout flow, a payout, or a treasury transfer. Under the surface, the operator is coordinating a stack of product, compliance, custody, asset, liquidity, orchestration, settlement, reconciliation, and support systems.

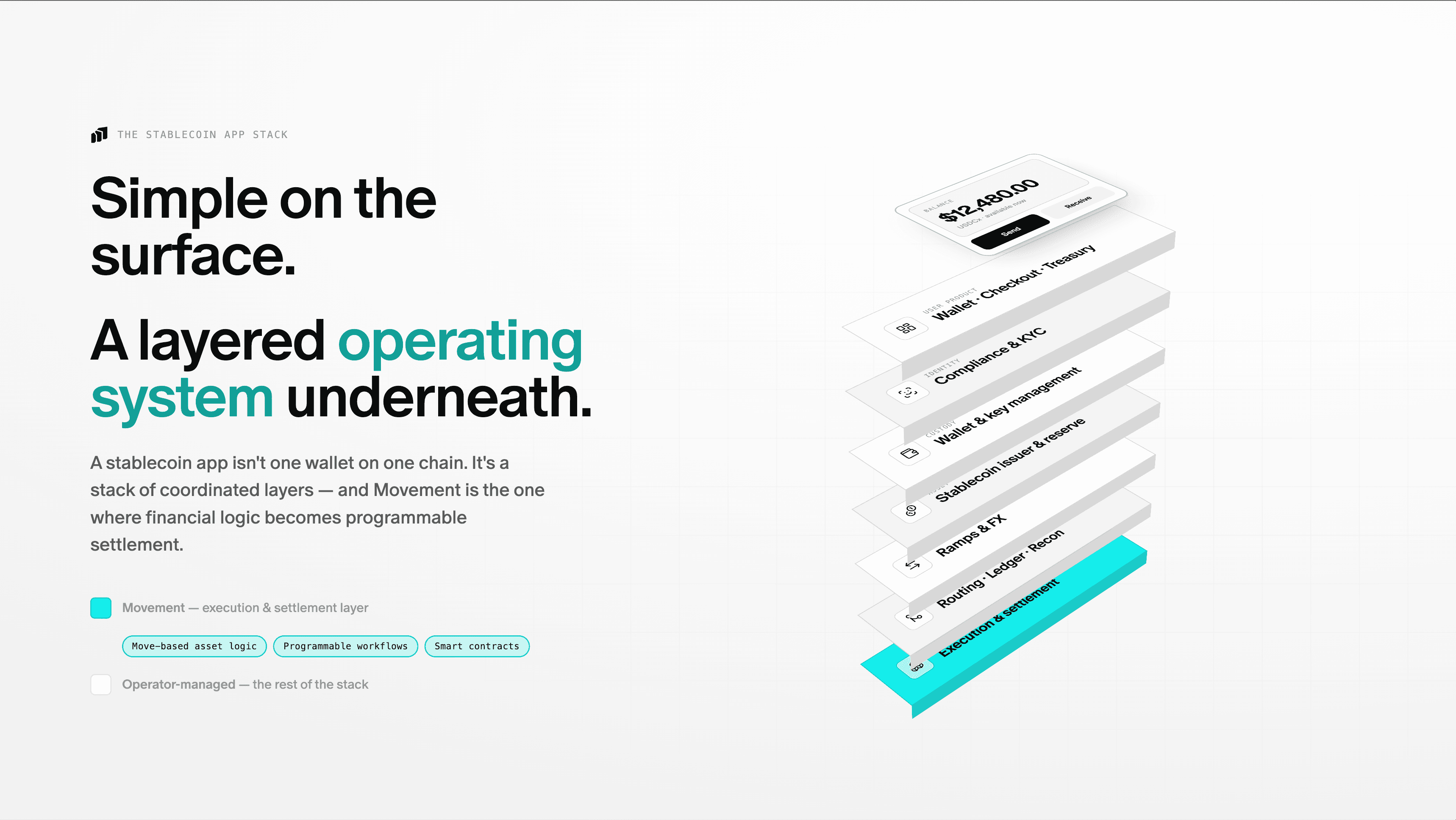

The stablecoin app stack includes the user product, wallet or custody layer, stablecoin asset, cash-in and cash-out ramps, liquidity and FX, compliance controls, transaction orchestration, settlement infrastructure, observability, reconciliation, and customer support. Infrastructure choices matter most where value-bearing state, permissions, settlement logic, and operational reviewability sit. This is where Movement provides the execution and settlement infrastructure layer, offering builders Move-based asset logic, programmable financial workflows, and application environments for stablecoin products, and vault infrastructure.

A stablecoin app is not one wallet on one chain

Most stablecoin apps are described by what the user sees: hold dollars, send dollars, receive a payout, pay a merchant, move treasury balances, or settle with a counterparty. That surface can feel familiar, especially when the app hides addresses, network choices, and token mechanics behind a fintech-style experience.

The operating reality is different. A stablecoin app is a stack. The user sees a balance. The operator manages identity checks, custody decisions, issuer exposure, local payment methods, FX, liquidity, transaction routing, settlement, ledgering, monitoring, failed-payment handling, and support.

That distinction matters because a blockchain or execution environment is only one part of the product. It can be a critical part, especially when financial state and application logic live there, but it is not the whole payments product.

What is the stablecoin app stack?

Figure 1. The stablecoin app is a stack, not one wallet on one chain.

A stablecoin app stack is the set of product, compliance, liquidity, and blockchain infrastructure layers required to let users or businesses hold, send, receive, spend, or settle value using stablecoins.

At the top is the user product: the wallet, account, merchant checkout, card experience, payroll flow, remittance app, or treasury dashboard. Beneath it sit identity and compliance controls such as KYC, KYB, sanctions screening, transaction monitoring, limits, and audit trails. The wallet and custody layer determines how keys, permissions, recovery, custodians, embedded wallets, MPC systems, smart accounts, or self-custody fit the product.

The stablecoin asset layer introduces another set of decisions: which issuer, reserve model, redemption path, supported networks, token standard, and risk model the product relies on. Cash-in and cash-out then connect the app to bank accounts, cards, local payment methods, mobile money, payment processors, or other payout systems. Liquidity and FX determine whether the product can convert value at acceptable spreads, in the right markets, at the right time.

Orchestration connects these layers. It may include transaction routing, batching, gas abstraction, retries, balance management, bridging where applicable, and workflow logic. The settlement and execution layer is where smart contracts, asset logic, and state transitions may live. Finally, reconciliation, observability, risk operations, and support help the operator understand whether the app ledger, on-chain transactions, fiat partners, and user-facing balances all match.

The front end, the money movement, and the operational truth are different systems

A consumer wallet, a fintech dollar account, a B2B settlement tool, and a developer protocol can all use stablecoins, but they do not expose the same stack to the user.

In a consumer wallet, the user may directly hold tokens and choose when to send them. In a fintech app, the user may see an account balance while stablecoins move in the background as a settlement or treasury rail. In a B2B flow, stablecoins may move between institutions, liquidity providers, or regional payout partners. In a protocol, smart contracts may coordinate escrow, fees, payout splits, collateral, or settlement events.

The product design question is not simply “which chain should we use?” It is “which parts of the product should users see, which parts should operators control, and which parts should infrastructure make reliable, auditable, and programmable?”

Where infrastructure choices matter

Infrastructure choices matter most where the app handles value-bearing state. Stablecoin applications need explicit rules for assets and balances. Transfers need predictable execution and clear failure handling. Developers need to reason about permissions, escrow, fees, limits, and settlement state. Operators need observability for accounting, compliance review, and incident response.

The execution layer is also where composability can matter. A product may need contracts that coordinate multiple actions: receiving a stablecoin, applying a fee, holding funds in escrow, releasing a payout, updating a settlement record, or exposing events to an internal ledger. If that logic becomes difficult to inspect or reason about, the rest of the app inherits operational risk.

This is the context in which Move-based infrastructure becomes relevant. Move’s resource-oriented model is designed around explicit handling of digital assets and ownership. For stablecoin app builders, that can help frame how assets, permissions, and state transitions are modeled in application logic. This should be understood as a developer and architecture benefit, not a guarantee that any app is automatically safe, compliant, cheaper, or free of operational risk.

Where Movement fits

Figure 2. Where Movement fits: programmable execution and settlement logic, bounded from issuer, wallet, ramp, compliance, liquidity, and support layers.

Movement fits at the execution and settlement infrastructure layer of the stablecoin app stack. It is relevant when builders need Move-based infrastructure for financial application logic: asset handling, permissions, balances, escrow, settlement workflows, and composable smart contract systems with secure vault infrastructure.

That role is important, but it is intentionally limited. Movement is not the issuer of the stablecoin. It is not the bank account, the on-ramp, the off-ramp, the compliance provider, the custodian, the liquidity venue, the payment processor, or the customer-support operation. Those layers still need to be selected, integrated, monitored, and governed by the product team.

Consider a global payout app like Zoth. A contractor signs up, passes the required identity checks, and receives a dollar-denominated payout from a platform. The app may show a simple balance and let the contractor choose whether to hold value, transfer it, or withdraw through a local payout method.

Behind that experience, the operator may need to accept funds from a platform, represent value in an internal ledger, convert or settle using a stablecoin, route the transaction through an execution environment, apply fees or escrow rules, connect to liquidity providers, and coordinate local payout. The operator also has to reconcile the app balance, on-chain movement, banking or ramp activity, support events, and any failed or delayed steps.

Movement’s role in that example would be the execution and settlement logic: the place where Move-based contracts can help model asset movement, permissions, escrow, and settlement workflows. It would not, by itself, solve KYC, local payout availability, FX liquidity, issuer risk, custody policy, or customer support.

Figure 3. User simplicity versus operator reality: stablecoin settlement is one step in a longer payout, liquidity, reconciliation, and support flow.

The hard parts are often at the edges

Strong settlement infrastructure does not remove the edge problems of stablecoin products. Cash-in and cash-out availability still vary by market. FX spreads and liquidity can decide whether a product is affordable to operate. Compliance obligations depend on jurisdictions, counterparties, product design, and the role of each service provider. Custody and key management determine who can move funds, recover accounts, or approve transactions.

Stablecoin asset choice also matters. Issuer, reserve, redemption, supported network, depeg, and governance risks should be evaluated directly. Operators need to understand whether users hold tokens, claims against an intermediary, or balances represented in an internal ledger. Those distinctions affect disclosures, support, risk controls, and legal analysis.

Reconciliation is another common failure point. A user-facing balance, an app ledger entry, an on-chain transaction, a ramp event, a liquidity trade, and a bank movement may all describe different parts of the same payment. If those systems do not reconcile cleanly, users may experience delays, support teams may lack answers, and operators may struggle with accounting or compliance review.

What fintech and crypto teams should evaluate

Before choosing stablecoin infrastructure, teams should map the product from the user action to final operational reconciliation. Who is the user? What balance do they see? Which stablecoin asset is used? Who holds custody? What identity and transaction controls apply? How does money enter and leave the system? Which liquidity partners support the required corridors? What happens when a transaction fails? Which ledger is the source of truth?

Only after those questions are clear should the team evaluate the execution layer. At that point, Movement is relevant if the product needs Move-based application logic for assets, permissions, settlement workflows, and composability. The stronger the financial logic inside the app, the more important it becomes for developers and operators to reason clearly about state transitions.

Strong stablecoin products make the stack legible to builders and operators while keeping unnecessary complexity away from users. Users should not need to understand every issuer, route, ledger, contract, and reconciliation step to receive value. Builders, however, do need that map.

Closing thought

Stablecoin apps are not just wallets, tokens, or chains. They are layered products that combine user experience, compliance, custody, assets, ramps, liquidity, orchestration, settlement, reconciliation, and support. Movement fits into that stack as execution, settlement, and vault infrastructure for builders who need Move-based financial application logic. Strong stablecoin apps hide the rail from the user while making the infrastructure legible to developers, operators, and compliance teams.

FAQ

What is the stablecoin app stack?

The stablecoin app stack is the set of layers required to let users or businesses hold, send, receive, spend, or settle value using stablecoins. It includes the user product, identity and compliance controls, wallet or custody layer, stablecoin asset, ramps, liquidity and FX, orchestration, settlement infrastructure, reconciliation, and support.

Where does Movement fit into the stablecoin app stack?

Movement fits at the execution and settlement infrastructure layer. It is relevant when builders need Move-based asset logic, programmable financial workflows, smart contracts, vault infrastructure, and settlement environments for stablecoin products.

Is Movement a stablecoin issuer, wallet, ramp, or compliance provider?

No. Movement should not be treated as the issuer, bank, wallet, custodian, on-ramp, off-ramp, compliance provider, liquidity venue, payment processor, or customer-support layer. Those functions remain separate parts of the stack.

What layers does a stablecoin app need besides a blockchain?

A stablecoin app usually needs a user product, identity and compliance checks, custody or wallet infrastructure, an asset and issuer model, cash-in and cash-out routes, liquidity and FX, orchestration, reconciliation, observability, support, and risk controls.

Why does the settlement layer matter for stablecoin apps?

The settlement layer matters because it can hold value-bearing state and execute application logic. It may define how balances, permissions, escrow, fees, transfers, and settlement events are handled. That makes it important for developers, operators, and risk reviewers.

How is a stablecoin wallet different from a stablecoin fintech app?

A stablecoin wallet often lets users hold and transfer tokens more directly. A stablecoin fintech app may show a familiar account or payment experience while using stablecoins behind the scenes for settlement, treasury, or payouts. The architecture, custody model, disclosures, and operational responsibilities can be very different.

What is the difference between stablecoin settlement and a completed payment?

A stablecoin transfer or on-chain settlement event can be one step in a payment flow. A completed payment may also depend on compliance checks, liquidity, FX, local payout, cash-out, user notification, and reconciliation between internal and external systems.

Why do liquidity and off-ramps matter in stablecoin apps?

Liquidity and off-ramps determine whether users or businesses can convert value when and where they need it. A product can have strong on-chain execution but still fail if spreads are too high, local payout is unavailable, or conversion depends on unreliable partners.

How can Move-based infrastructure help stablecoin app builders?

Move-based infrastructure can help builders model assets, ownership, permissions, and state transitions explicitly in application logic. For stablecoin apps, that is relevant to balances, escrow, fees, settlement events, and composable financial workflows.

Does Movement make stablecoin apps automatically compliant or risk-free?

No. Compliance, risk controls, custody, asset selection, liquidity, disclosures, support, and jurisdiction-specific obligations remain separate product and operational responsibilities. Movement’s role is infrastructure for execution and settlement logic, not a guarantee of compliance or risk removal.

What should fintech teams evaluate before building on stablecoin infrastructure?

Teams should evaluate the user experience, custody model, stablecoin asset and issuer risk, cash-in and cash-out routes, liquidity and FX, compliance obligations, ledger design, support model, failure handling, and reconciliation process before choosing the execution layer.

What parts of the stablecoin app stack should users never have to see?

Users should usually not have to understand every contract, route, ledger entry, liquidity provider, gas mechanic, compliance workflow, or reconciliation step. Builders and operators need that visibility so the product can feel simple without hiding operational risk from the team.